Authors: Iva Nenadić and Marko Milosavljevič

There are many conceptual distinctions and approaches in measuring media pluralism but most of them, if not all, consider the concentration of ownership in media markets. Concentration of media ownership is seen as one of the biggest threats to media pluralism as it may narrow the diversity of editorial voices and information. This understanding has, as well, been employed in the Media Pluralism Monitor (MPM)[1] – a project that evaluates conditions for media pluralism in all EU member states as well as candidate countries. The MPM, unlike many other attempts to evaluate this phenomenon, does not look at the market dimension only. It considers market plurality as one of the four areas that determine the conditions for media pluralism in a given country (the other three areas are: Basic Protection, Political Independence and Social Inclusiveness). However, the conditions and the composition of players in the media markets have seen profound changes over the last decades in ways that potentially affect plurality and diversity. Thus, the understanding of what the media market is and which are the measures to assess its pluralism should be re-considered. This paper attempts to take a step in this direction.

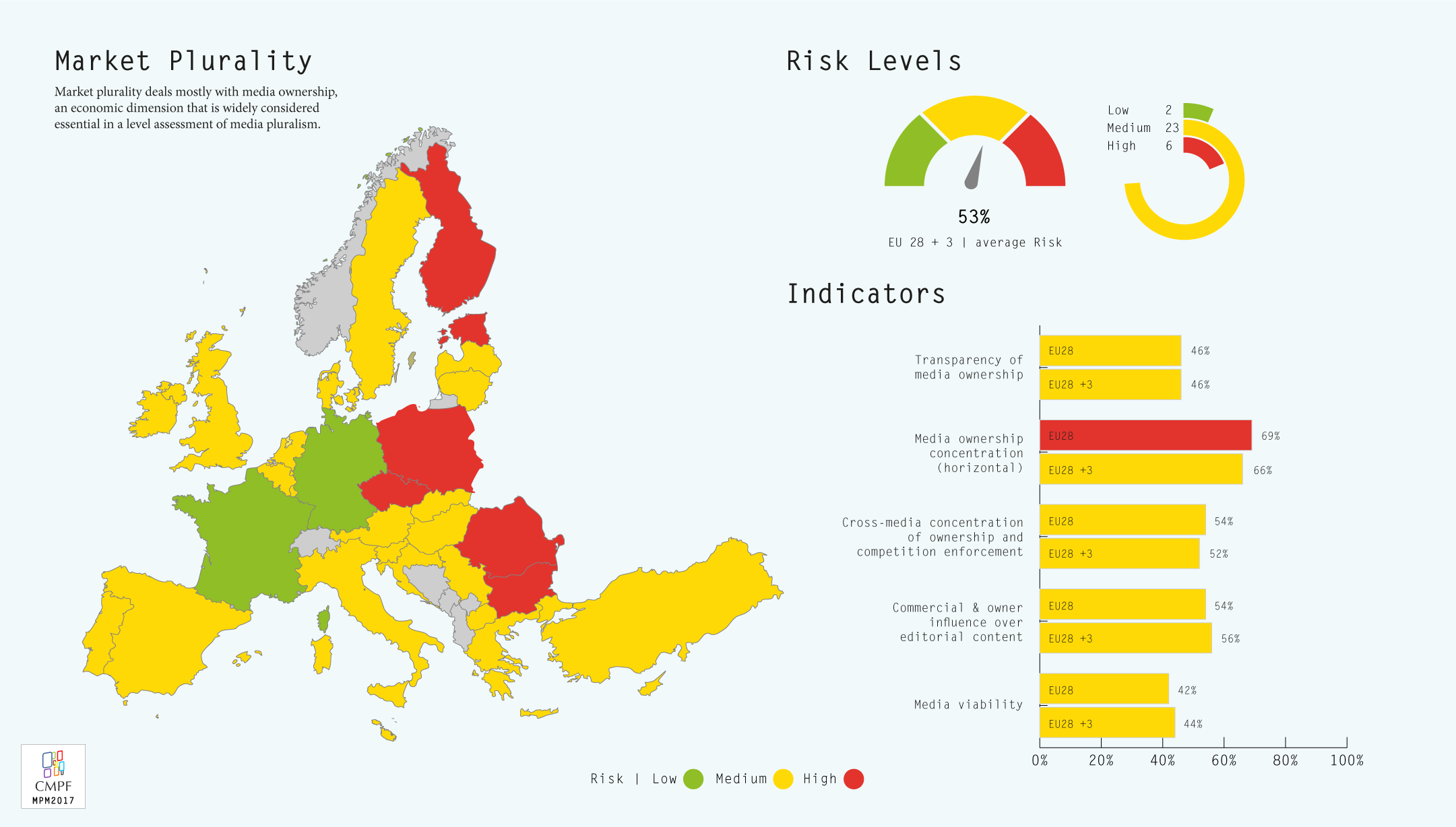

Media markets are often seen as two-sided markets (see: Anderson and Gabszewicz, 2006): providing (or selling) information to citizens and selling the citizens’ attention to advertisers. They are specific markets and the media business is a specific business, containing both economic and democratic value. Media business depends on the interest of the public and, at the same time, justifies its unique position within the public interest. Considering that media content is relatively cheap to deliver but much more expensive to produce, media business rationale has a tendency towards concentration – while competition is perceived as crucial for pluralism. Four main types of media concentration are elaborated by scholars and addressed by regulators: horizontal – mergers within the same market; vertical – concentration of different production levels; diagonal or cross-media ownership – across different media types; and conglomerate – when an enterprise from outside media sector buys media assets (Bardoel and van Cuilenburg, 2008). The MPM, in its current form, covers two types of media concentration: horizontal and cross-media, considering also (to some extent) the concentration of internet service providers (ISPs) and internet content providers (ICPs). The Monitor assesses the actual level of different types of concentration – of both revenue and of audiences – based on the “four-firm (or Top 4) concentration ratio” (CR4). Another commonly accepted measure of market concentration would be the Herfindahl-Hirschman index (HHI) which is calculated by squaring the market share of each firm competing in a market and then summing the resulting numbers.

So far, The results of the MPM show that most countries in the EU, within their media policy, have enacted certain limits or thresholds on horizontal concentration in traditional media markets to ensure sufficient plurality and diversity. Specific safeguards to prevent cross-media concentration are less common, but in those cases general competition laws (antitrust and merger control) may also apply and take sufficient account of media pluralism. Market positions of digital intermediaries and platforms that do not produce content of their own but serve as delivery channels, have currently not been taken into account with the same approach.

The experience of the MPM, and the changing realities, require a more nuanced method of measuring, as well as additional aspects and actors to be measured. One of the matters that potentially deserves a deeper look is the concentration of distribution networks and the (dominant) (new) intermediaries which increasingly influence or determine the conditions for access to, and the nature of, the media and content. As mentioned, the MPM already takes into account the concentration of the ISPs which provide internet connection, but could further consider the market positions of hosting companies, search engines and social media platforms. The latter are of particular importance due to their economic strength, global reach and the role they play as a pathway to news (see: Martens et al., 2018) and in politics (think of political campaigns). Despite them not being media in a traditional sense (i.e. not producing content of their own), they perform certain media-like functions: acting as gatekeepers (Milosavljević and Broughton Micova, 2016) or social editors (Helberger, 2017) by prioritising and personalising the content on offer; and providing a public sphere, even if “the vision of a singular, integrated public sphere has faded in the face of the social realities” (Dahlgren, 2005: 152). Another reason to consider search engines and social media platforms in assessing the conditions of market plurality comes from the fact that they are competing with media companies for the same slice of online advertising expenditures – and winning this game, leaving traditional media with the crumbs (see: Rose, 2018). This comes as no surprise since no media outlet (at least not known to the authors of this piece) has ever been able to reach almost a third of the world’s population, which Facebook does with its 2.27 billion monthly active users (Facebook, n.d.). Another source of competitive advantage that search engines and social media platforms have over traditional media companies are data – the large amounts of data they collect on individual’s personality traits and preferences which allow them to provide targeted and potentially more effective advertising.

With all this in mind, to assess the levels of market concentration of traditional media companies without considering the role and impact of other players, would be discrepant to the current realities. Therefore, the Monitor needs to advance its understanding of who the players operating in the media markets are, which safeguards and conditions are inevitable for pluralism, and which are the methods to evaluate this news setting and power relations – as the old measures of CR4 and HHI are clearly not designed to consider the logic and motivations of the largest technology platforms who are less competing IN the market but rather FOR the market. This means that it could be less about the number of companies, and more about number of choices people have (e.g. first to understand how news is being delivered to them via online intermediaries, and then to be able to choose or to shape the algorithm of their news feed/recommendation system). Not that the focus on external pluralism (number of different companies competing in the media market) should be dismissed, but a focus also on internal pluralism within these platforms should be added – perhaps through the measures of algorithmic transparency: vis-a-vis public authorities and vis-a-vis public.

[1] The MPM is coordinated by the CMPF and co-funded by the EU

References:

Anderson, S. P. and Gabszewicz, J. J. (2006) “Chapter 18 The Media and Advertising: A Tale of Two-Sided Markets”. In: Victor A. Ginsburg and David Throsby (eds.) Handbook of the Economics of Art and Culture, Volume 1, Elsevier B.V. (pp. 567-614) https://doi.org/10.1016/S1574-0676(06)01018-0

Bardoel, J. L. H. and Cuilenburg, J.J. van (2008) “Media and communication markets”. In: P. Fourie (ed.) Media Studies Volume 2: Policy, Management and Media Representation. Cape Town: Juta. ISBN: 9780702176753 (pp. 119-154)

Dahlgren, P. (2005) The Internet, Public Spheres, and Political Communication: Dispersion and Deliberation. Political Communication, 22 (2): 147-162. https://doi.org/10.1080/10584600590933160

Facebook (n.d.) Number of monthly active Facebook users worldwide as of 3rd quarter 2018 (in millions). In Statista – The Statistics Portal. Retrieved January 28, 2019, from https://www.statista.com/statistics/264810/number-of-monthly-active-facebook-users-worldwide/

Helberger, N (2017) Facebook is a new breed of editor: a social editor. Media Policy Project blog, London School of Economics and Political Science. Retrieved from: https://blogs.lse.ac.uk/mediapolicyproject/2016/09/15/facebook-is-a-new-breed-of-editor-a-social-editor/

Martens, B.; Aguiar, L.; Gomez-Herrera, E. and Mueller-Langer, F. (2018) The digital transformation of news media and the rise of disinformation and fake news – An economic perspective. Digital Economy Working Paper 2018-02. JRC Technical Reports.

Milosavljević, M. and Broughton Micova, S. (2016) Banning, Blocking and Boosting: Twitter’s Solo-Regulation of Expression. Media Studies, 7 (13): 43-57. https://doi.org/10.20901/ms.7.13.3

Rose, J. (2018) Facebook and Google dominate online ads. Can alliances between news publishers compete?. Poynter (May, 24). Retrieved from: https://www.poynter.org/business-work/2018/facebook-and-google-dominate-online-ads-can-alliances-between-news-publishers-compete/

NOTE: The first version of this paper, titled “Adapting the media pluralism definitions to the new digital realities”, was presented ECREA’s 7th European Communication Conference (ECC) “Centres and Peripheries: Communication, Research, Translation” held in Lugano, Switzerland, October 31-November 3, 2018. The paper was part of the panel on: “Making and breaking media plurality – lessons from the Media Pluralism Monitor”.

{kind=link}